Bets Against

US stocks closed lower on Tuesday, with the S&P 500 down 0.4%, snapping a six-day winning streak.

The Nasdaq slipped 0.4% as well, while the Dow Jones lost 114 points.

However, sentiment turned cautious amid renewed uncertainty around trade negotiations and political resistance to the tax plan.

A broad tech selloff weighed on markets, with Alphabet (-1.5%) falling after its Google I/O event and declines in Nvidia (-0.9%), Meta (-0.5%) and Apple (-0.9%).

Tesla bucked the trend, gaining 0.5% after Elon Musk confirmed he plans to remain CEO for the next five years.

In my May 09, 2025 note, in expectation of a Moody's downgrade of U.S. credit, we looked back at the 2011 downgrade by Standard and Poors.

At the time, with the economy still wobbling from the global financial crisis, most expected the S&P downgrade to trigger capital flight OUT of U.S. assets (particularly Treasuries).

It was just the opposite. Why? The U.S. downgrade forced investors to scrutinise global sovereign debt. That pressure amplified the stress that was already present within some weak spots in global bond markets.

Over the next half year of so, Europe was taken to the brink of sovereign defaults – averted only by the European Central Bank's promise to do "whatever it takes" to save the euro.

Fast forward to today, global government indebtedness is significantly worse than it was in 2011.

Once again, we should expect focus to turn to Europe, where weak spots like France are already burdened by debt levels well above 100% of GDP, and with stall speed economic growth. Add to that, the European Commission is now compounding the debt problem - committing to a massive fiscal spend on defence and AI, to be funded by more deficit spending. That means even more debt for the constituent eurozone countries.

And it looks like Japan may get the spotlight this time, too. The very long end of the bond market is trading like a debt reckoning is coming - in a country that remains the most heavily indebted developed economy in the world.

What about this?

Unlike Europe and Japan, the U.S. has a plan to meaningfully grow the denominator in that ratio. Still, the bets against that plan are clearly manifesting in this chart ...

Also manifested in this chart above are bets that the central banks will return to QE (return to buying their own bonds).

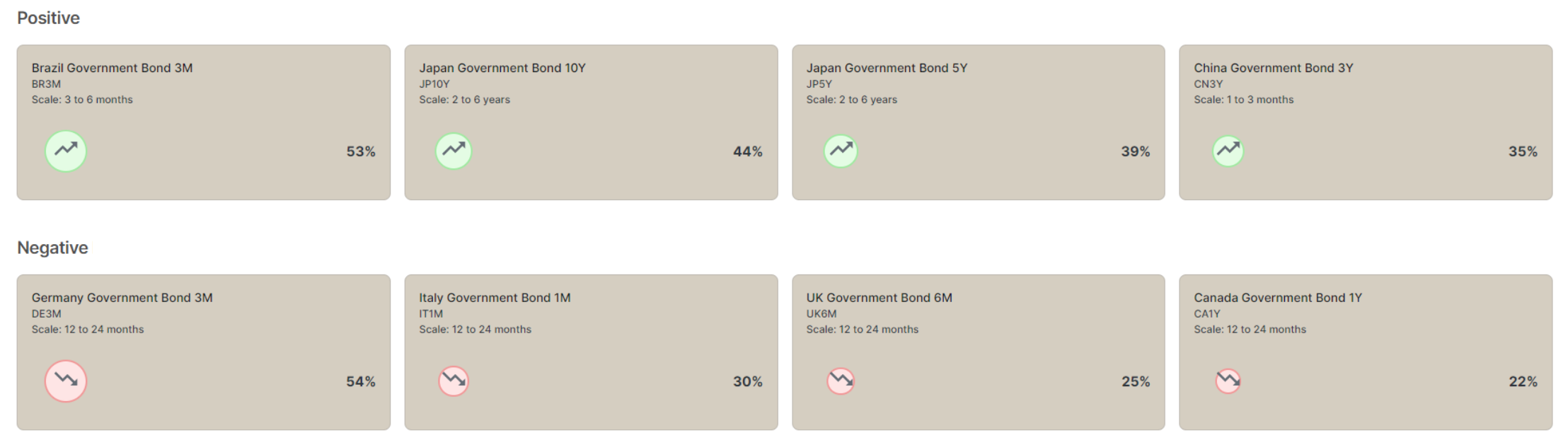

Global Trend Report | March 2025

Access our dynamic approach to stay ahead of trends and crashes. We highlighted the bullish long-term (2-6yrs) trend at 44% in Japanese 10y Government Bonds in our March Global Trend Report (summary table shown above), whilst pointing out the 100% trend score in the 3-6m trend range as a likely market top – materialising as a 30% drop!