Bears Squeezed

Macro Perspectives

The stock market bears have officially been squeezed to the point of capitulation.

By setting low expectations, they've manufactured the conditions for their own pain, which has come in the form of positive surprises in both economic growth and corporate earnings.

Many of the recession calls have been abandoned over the past week, and instead, there is now acknowledgement of:

the power of excess money supply still sloshing around the economy.

the power of extravagant government spending programs, still in the early stages of deployment.

Meanwhile, the inflation catalyst (the 2020-2021 growth shock in money supply) is over. Even with oil prices rising, the normalization of growth in money supply (if not contraction in money supply) should keep the risk of another surge in inflation off the table.

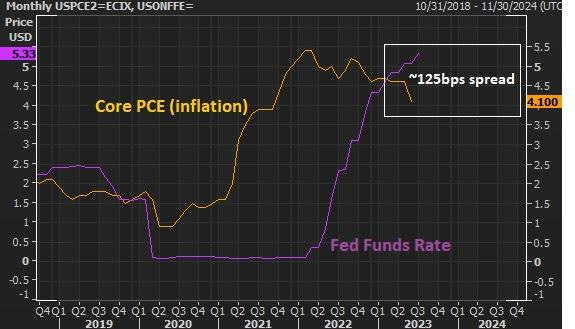

Add to that, the Fed now has plenty of "insurance," to the tune of about 125 basis points, against a core PCE that has now fallen to 4.1%. This presents a risk, to the bears, that a rate cut could be the next move made by the Fed.

The bears have been on the wrong side and they are looking for opportunities to play catch up to a benchmark index (S&P 500) that's up 20%.

We talked about this earlier in the month. The easy targets (the laggards), in this case, are small cap value stocks and commodities. On the former, the small cap value ETF (IWN) is breaking out.

On the latter, both oil and copper have broken out of downtrends; Oil is up 20% since late June, Copper is up 8%. Here's the latest look at copper . . .

And by the end of this week, we may have all Western world central banks on hold, marking an end to the interest rate cycle.

This tends to reverse capital flows back toward emerging market economies. Given that emerging market stocks have been underperformers/laggards, it's a target for those in the investment community looking to catch up.

PS: If you know someone that might like to receive my daily notes, they can sign up by clicking below.