As we discussed yesterday, earnings estimates have been dialed down, with Wall Street expecting a 6.7% contraction in S&P 500 earnings for Q1, in a quarter where the Atlanta Fed is tracking GDP growth at 2.5%.

We'll get an update to that Atlanta Fed growth projection today.

We'll get the first government estimate for Q1 GDP on Thursday.

There is potential here for someone to be wrong.

At the moment, it looks like it's Wall Street - yesterday was another day of big positive surprises on the earnings front. And in many cases, revenues have come in higher than expectations too.

Microsoft. 3M. Google. Biogen. Chipotle. GE. McDonald's. Kimberly Clark. Visa. GM. Haliburton. Pulte.

The broad economy is well represented in these stocks - all beat earnings and revenue estimates. For a preview of earning’s for the day, click on the Earnings Chartbook attached below:

It was a record quarter for Chipotle. Microsoft, a $2 trillion company, had record revenue and record net income. Pulte Homes grew revenue by 12% compared to Q1 of last year, with 28% EPS growth ... despite being faced with the fastest doubling in mortgage rates on record.

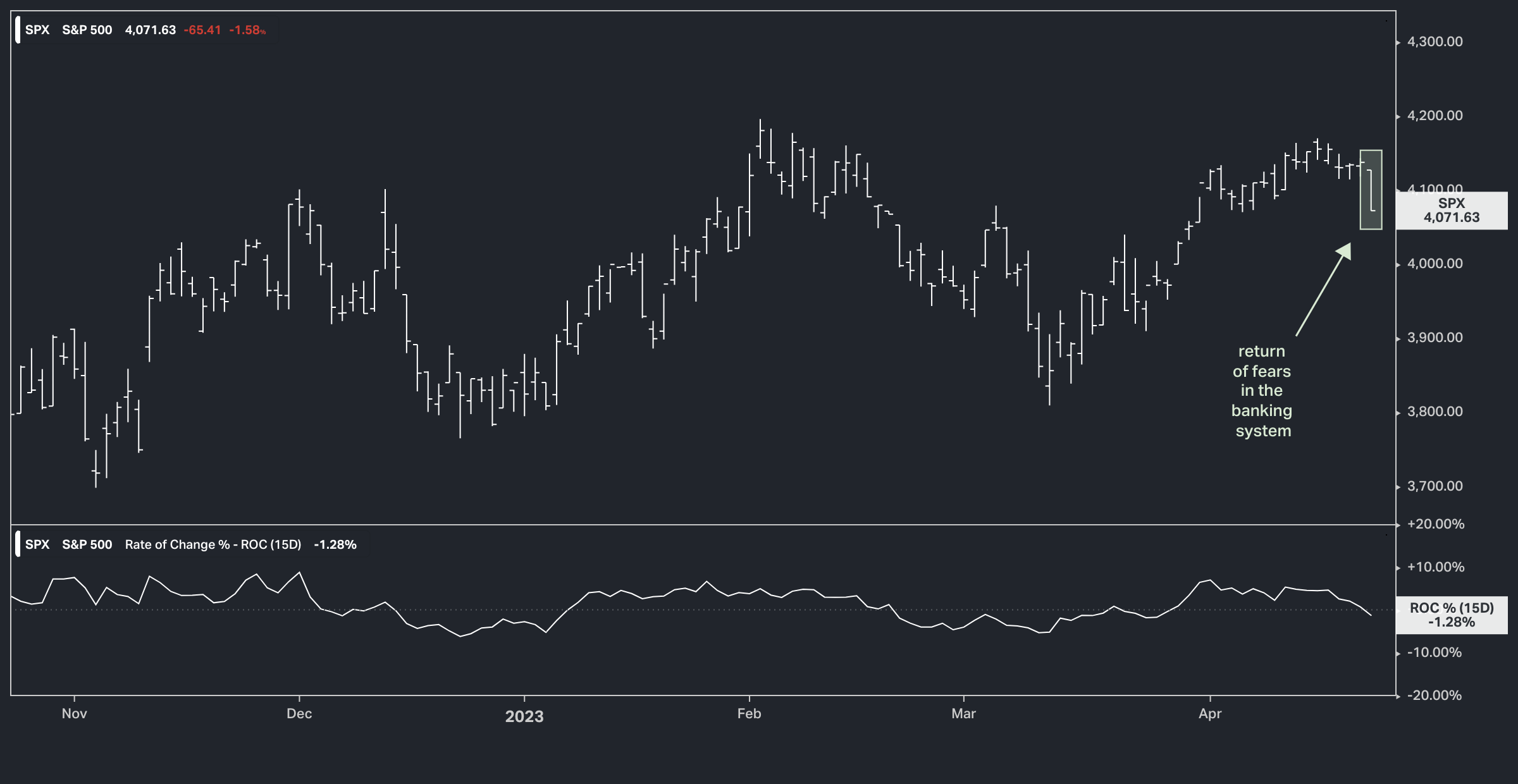

This all sounds pretty good. What about the renewed fears surrounding banks that led to this . . .

Remember, First Republic Bank (FRC) was one of the three vulnerable banks (high uninsured deposits, large duration risk) that were harmed by a run on deposits last month. Two failed, but FRC was preserved via an infusion of deposits from a consortium of big banks (arranged by the Treasury). They reported yesterday after the close, and divulged the exit of half of depositor assets in the run (excluding the Treasury arranged infusion).

With that, stocks (and interest rate markets) behaved today as if a banking shock might be turning into a banking crisis.

But remember, the Fed is back in the business of expanding the balance sheet (QE) - they've given banks unlimited access to short term liquidity to meet demand of depositors (a crisis averting backstop).

That said, after doing nearly $400 billion of QE in March, as the fears quelled, the balance sheet shrank for the past four consecutive weeks (as you can see in the chart below, to the far right).

After yesterday's events, I suspect we'll find the balance sheet is expanding again.