Bad News is Good News...

Macro Perspectives

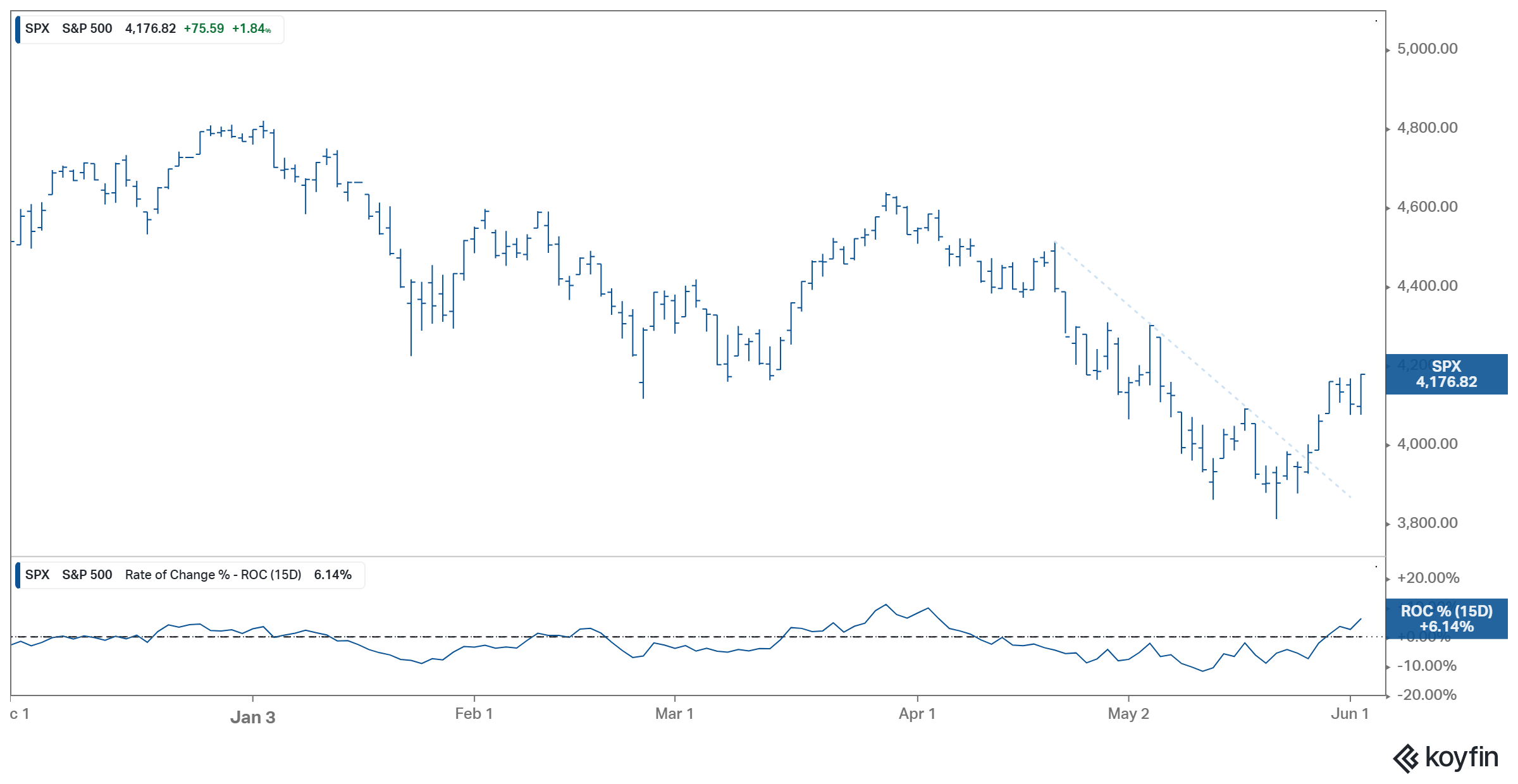

Last Thursday (26 May), we talked about the setup for a break of the trendline in this chart below - moreover, we were looking for a close above the 4,000 level in the S&P 500, as a bullish signal for stocks.

We got it, and we've since had about a 5% rally in stocks.

This, as we head into a big government jobs report today.

What should we expect?

We had some clues from the private jobs report yesterday morning, published by ADP - the jobs added in May came in at 128k, versus the market consensus of 300k. It was a miss.

For today's report on non-farm payrolls, the expectation is for the weakest report in over a year, at 325k jobs added.

To be sure, this will be one of the more important jobs reports we've seen in a while.

Why? Because the Fed has explicitly targeted jobs, in the effort to bring down inflation. The Fed Chair, Jay Powell, told us explicitly that they intend to bring the ratio of job openings/job seekers down from two-to-one, to one-to-one.

Yes, we have a Fed that is trying to manipulate to the goal of higher unemployment.

In my career in markets, I've never witnessed a Fed that is explicitly attempting to destroy demand and jobs…but here we are.

With that, we are in a bad news is good news stock market.

As we've discussed here in my daily notes, the more verbal influence that the Fed can have on markets, and consumer and business psychology, the less work that the Fed has to do with interest rates. The shallower the path of interest rate hikes, the higher the probability of a soft landing for the economy. That's a slowing growth scenario (the best case scenario in the current environment).

On that front, so far so good. The markets are doing the Fed's job for it. Lower equity valuations, higher gas prices and higher mortgage rates have quickly changed consumer and business psychology. Demand is coming down, which should translate into some loosening in the job market.