The U.S. bond market was closed on Monday. Yet we entered yesterday with a spike back to the dangerous 4% level in the 10-year yield.

It was just two weeks ago that the combination of the global benchmark for interest rates (U.S. 10-year Treasuries) at 4% and the global benchmark for stocks (the S&P 500) back at the lows of the year, was creating stress in the global financial system. It looked like a breaking point.

And it was: The next morning, the Bank of England (BOE) was forced to rescue failing UK pension funds.

As Warren Buffett has said, "only when the tide goes out, do you discover who's been swimming naked." The "tide" in this case, is the easy money, low inflation era.

With higher rates, UK pension funds have been exposed as overleveraged and dangerous to the UK government bond market. As the value of UK government bonds (gilts) were falling (rates rising), these funds were getting margin calls, where they were forced to sell bonds. The forced selling, resulted in lower bond values, which resulted in more margin calls, which resulted in more bond selling (and a self-reinforcing global sovereign debt spiral was underway).

It has now been revealed that these massive pension funds were just hours from insolvency, which would have quickly spilled over into the UK financial system, which would have quickly become a problem for the global financial system, and global sovereign debt markets.

With that, we closed the day yesterday with a very important comment from the head of the Bank of England.

There has been speculation that the BOE will continue to absorb the stress in the pension funds, and whatever else it might emanate in the financial system - for as long as it takes. But the BOE Governor rejected that - warning the pension funds that they have three days to fix themselves, using the liquidity provided by the BOE.

This comment sent U.S. markets back to the worst levels of the day, and back around the danger levels of two weeks ago.

This comes as the Fed continues to march officials out in front of the media with hawkish rhetoric.

This comes just two days ahead of the very important U.S. CPI number.

So, the current level of global market interest rates are already proving to create stress in the global financial system. Meanwhile central banks (led by the Fed) continue to talk about responding to hot inflation data, with even higher rates.

What if the inflation data on Thursday is hot?

Keep this in mind: The Bank of England (and the Fed) are responsible for maintaining stability* in the financial system.

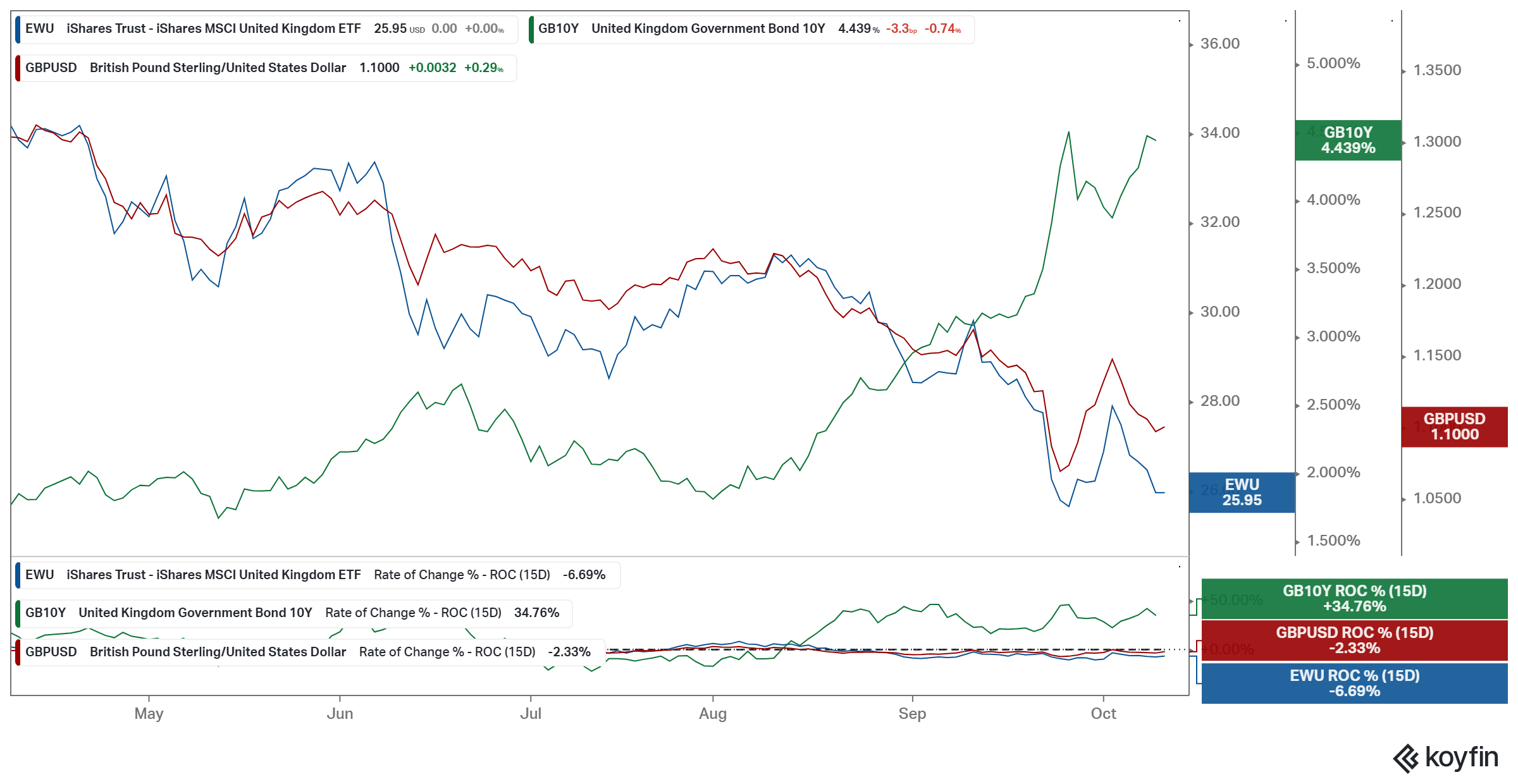

*please see bond roc’s in the charts provided for proof of lack of stability.

The BOE is talking to UK pension funds as if they are in a position of strength. They are (BOE), right now, the "buyer of last resort," in the UK bond market - they are in a position of weakness.

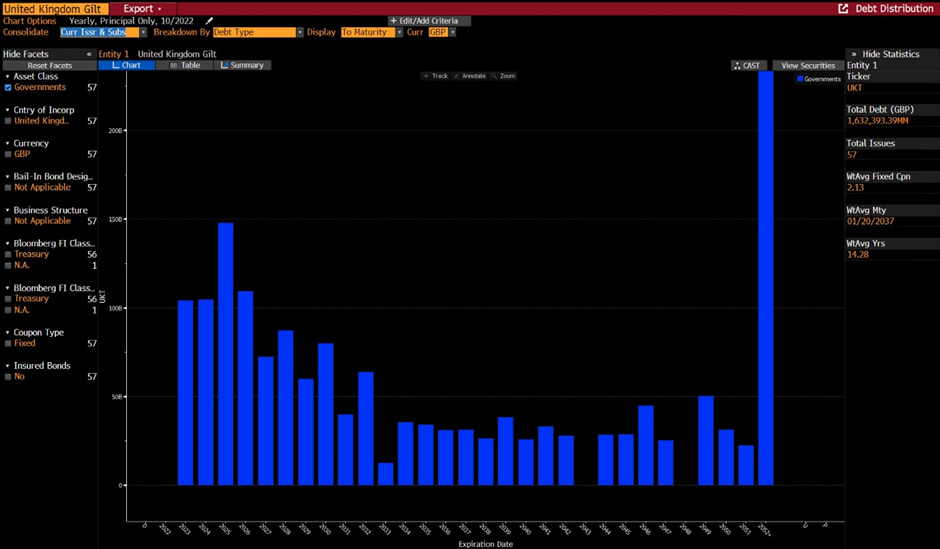

30 year gilts represent the majority of the U.K.’s debt profile - we can expect to see an unwind of the largest portion of the gilts market . . . in three (3) days.

We've seen what that looks like - the BOE have been forced to come off of the sidelines, and return to the business of emergency policies (QE).

“If you owe the bank $100, you have a problem. If you owe the bank $100 million, the bank has a problem”.