A Stable Housing Environment

Macro Perspectives

We had strong housing numbers yesterday morning.

Housing starts jumped, though off of the lows of the past year. The decline (to those lows) was driven by the Fed's historic interest rate hikes, which (related) caused the quickest doubling of mortgage rates on record

With that formula, following the post-covid boom in housing prices, the housing market has been a subject of "bubble talk." Let's take a look.

First, here's a look at building permits.

Here's a look at housing starts - in May this was running at the hottest rate in seven years . . .

Now, from these two charts you can see the direct impact of rising interest rates on home building. We can also see, on the left side of the charts, what a housing bubble (and burst) looks like.

If we look back at that 2006 period, home builders were building at about a 40% hotter pace, with about 10% less population.

That real estate bubble was primarily driven by credit agencies AAA stamping high risk/high yielding mortgage portfolios (a mix of fraud and incompetence on the part of the ratings agencies). With a AAA rating and a high yield, massive pension funds had no choice, if not an obligation to plow money into those investments. With that insatiable demand, mortgage brokers and bankers were incentivized to keep sourcing them and packaging them.

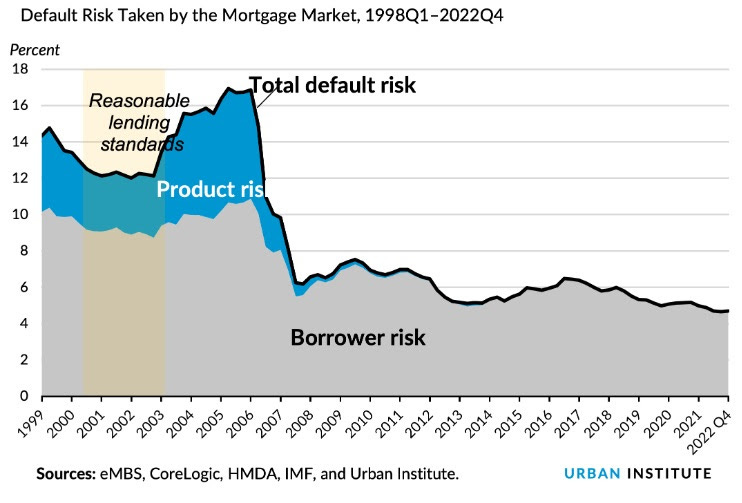

This post-covid housing environment was much different and much less vulnerable to rate hikes. The graphic below shows a different risk profile, which aligns with the current environment of high creditworthiness (low debt service) and stringent lending standards (post-financial crisis).

We discussed these housing market comparisons in my December 14th note in 2021 ( here ), as we were a few months away from the Fed's rate liftoff.

With that, I said . . . "What looks likely, in the face of a rate tightening cycle, is that real estate prices just stay persistently high, and even continue higher - driven by multi-decade high economic growth, massive new money supply floating around, and a very tight labor market. At higher rates, it will just cost more to live."

This aligns with what we've discussed throughout on the inflation topic: "rate-of-change" in prices will slow, but the level of prices is here to stay.

It's by design: inflate asset prices and inflate away the value of debt.

I’ve done the research, dug deep into the building process of this new economy, and identified the companies that are leading the charge in Generative AI. These are the guys with cutting-edge technologies, innovative business models, and visionary leadership. They’re at the forefront of transforming industries and shaping the future.

Become a member below, places are limited, to gain exclusive access to in-depth research, expert analysis, and timely investment recommendations focused on the Generative AI revolution. Allowing you to build a sophisticated, targeted, portfolio.