A primer to today's Job's Report

Macro Perspectives

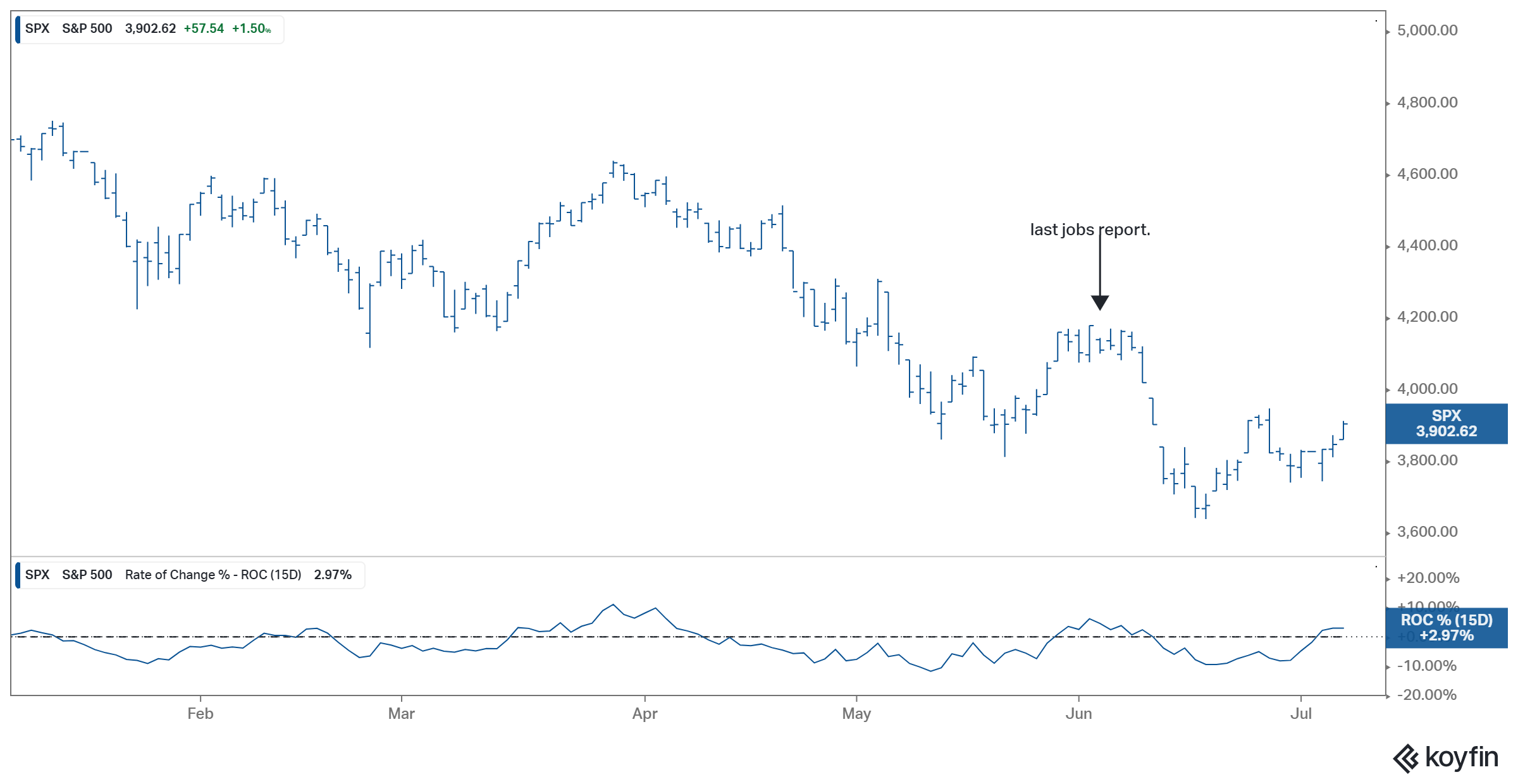

We get the June jobs report today.

To recap, the Fed has explicitly targeted employment as a tool to bring down inflation. The last jobs report (measuring May employment) wasn't weak, but it wasn't strong and the wage component was relatively soft. Stocks moved lower following that report. And we haven't seen that pre-jobs number level since.

The consensus estimate for today's number is for 268k new jobs added - that would be the weakest job growth since April of last year. The six month moving average is over 500,000 monthly jobs added.

So a number today in the 200s would indicate a less healthy job market (still good, relative to pre-pandemic times).This less healthy jobs report would reflect an economy that is likely in recession.

Is bad news good news? Will it curtail the Fed's interest rate threats? Probably. That said, the Fed has been focused on getting people back into the job market, and reducing the massive number of job openings - shaking out the excesses of an exuberant economy. On that front, as you can see in the chart below, the report on Wednesday this week on openings showed things rolling over (albeit very gradually)...

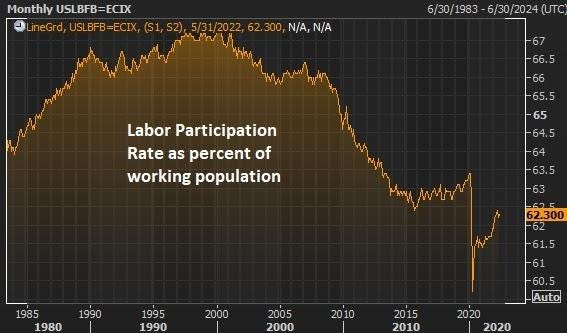

Now, let's look at the labor participation rate - we haven't recovered to pre-Covid levels and well under the levels of past decades...

Still, if we look at the math on how that gap between job seekers and job openings will close, it doesn't look possible. It's a big gap (over four million people). That said, the Fed's primary objective is to reduce the leverage of the job seeker, and current workers, to command high wages.

Why? Higher wages are fueling inflation.

If we look at the record low levels of consumer confidence, they've probably already accomplished that goal.