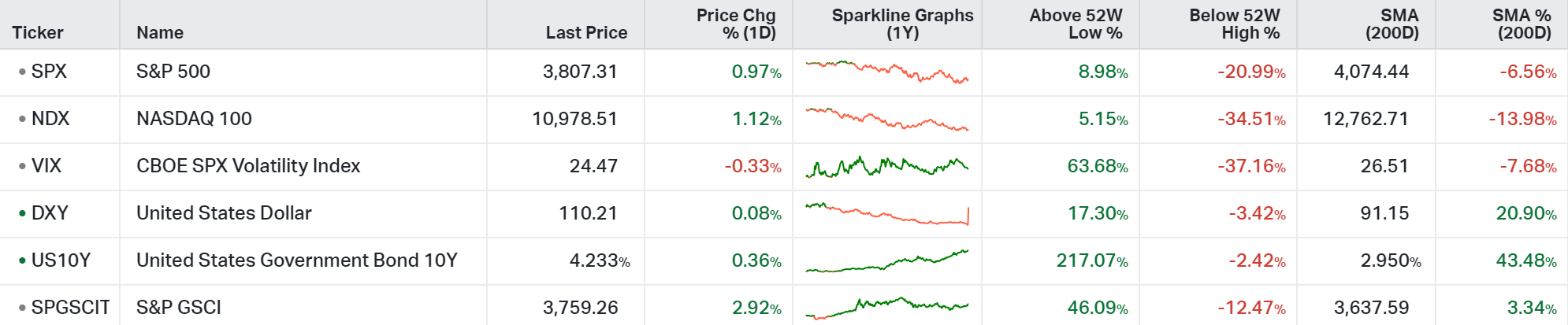

A power shift in Congress and dollar's decline.

Macro Perspectives

U.S. midterm elections take place today.

The odds continue to heavily favor a power shift in Congress, with a 70% chance of a Republican sweep of the House and Senate (according to the betting markets at PredictIt).

The notable market mover in the past two sessions has been the dollar, lower. Let's take a look at the dollar chart ...

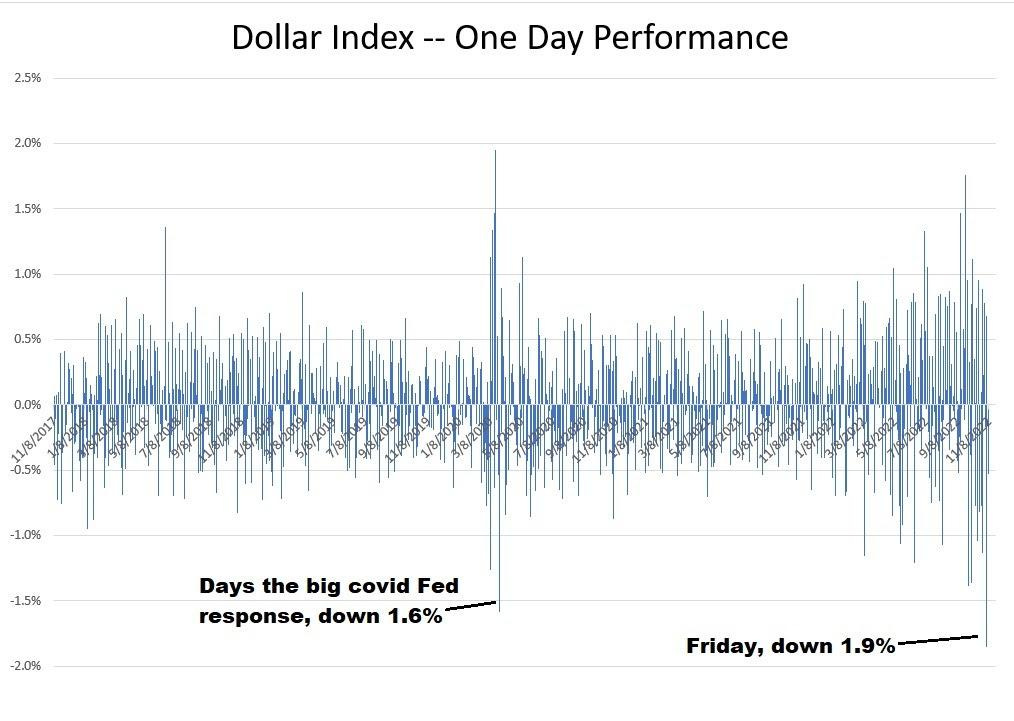

The dollar was down 1.9% on Friday. It was down another half a percent yesterday. As you can see in the chart, Friday has some interesting recent comparables - both big central bank intervention days. If we zoom out five years, we find that Friday was the biggest down day in the dollar.

This five-year look at daily change in the dollar index includes the massive fiscal and monetary response to covid lockdowns as well as the very contentious U.S./China trade war.

So what could trigger a bigger dollar decline on Friday, than all of the events mentioned above?

Was it anticipation of gridlock in U.S. Congress and therefore an end to the excessive fiscal spending, which softens the inflation and rate outlook?

Was it Friday's jobs report, which showed some weakness, and could give the Fed reasons to slow down or pause on rates in December?

Was it Xi's speech at the China International Import Expo on Friday, where he said China remained committed to opening up to the outside world? It's global supply positive (helps with supply related inflation pressures). And it's global growth positive, which could reverse some of the flight to safety that has been driving the dollar higher.

Maybe all of the above have contributed to this move in the dollar, which looks like maybe early stages of a trend change (to lower dollar).

NB: Within The Gryning Portfolio, we are Short $DXY.

PS: Would you like to manage your money in an institutional-grade portfolio based on the views expressed in The Gryning Times? Click below.