A (potential) Positive Catalyst

Macro Perspectives

We get June inflation data on Wednesday and Q2 earnings will kick off later in the week with the big banks.

The "base effect" of the consumer price index has been telegraphing a cliff dive in this coming headline inflation number for several months. I'm seeing a consensus view on the monthly change at 0.3% - if that's the case we might get a sub 3% number (like 2.95%).

Now, this is the "headline" number. The Fed, of course, is looking at core PCE, which measures the change in prices of goods and services that people have actually paid -- not just a selling price. "Core," of course, strips out food and energy prices.

Still, we shouldn't underestimate the appetite of the media and the White House to celebrate this headline inflation number on Wednesday. They will, especially if it breaches 3%.

It may also (positively) influence confidence, which has been running near crisis-low levels. For perspective, a year ago, we were at peak inflation. Small business optimism had plunged to nine-year lows, and consumer sentiment was on record lows. It was all driven by 40-year high inflation, and a Fed that was talking down stocks and vowing to destroy jobs.

Now we may get an inflation print under 3% (a third of the rate of change of a year ago). The Fed meanwhile, while continuing its chatter about an insurance hike (or two) is no longer threatening stocks and jobs.

The correlation between inflation and confidence is a tight one.

With the above in mind, the inflation data this week should be a positive catalyst for confidence (good for markets).

GRYNING | AI: This is where you gain access to state of the art, institutional grade analysis - analysing +10,000 features per day per stock and rating stocks probability of beating the market with the AI Score.

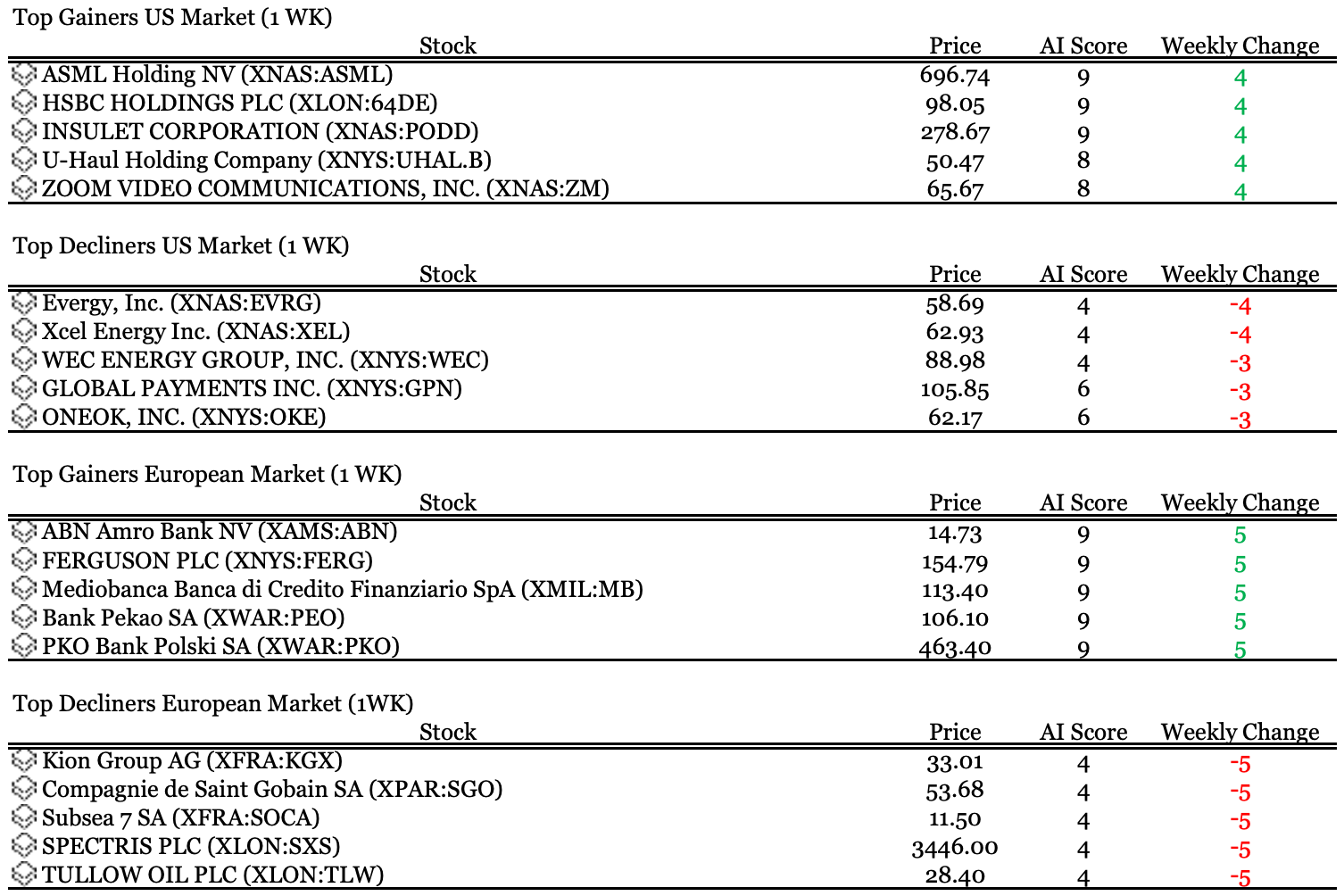

Top Weekly Movers - Stocks with the biggest AI Score change compared to 1 week ago.