A Good Second Half...

Macro Perspectives

Standard and Poor's published its Purchasing Managers' Index report Friday morning. This is a "flash report" projecting the way July private sector output is tracking.

It wasn't good - the index fell from 52 to 47 (weighed down by services, not manufacturing).

Below 50 is considered to be a contraction in activity, which tends to be consistent with a contraction in the economy. This has people talking about "possible" recession…my thoughts on the matter differ, the economy has very likely already been in recession - for the first half of the year. It's old news.

Official GDP contracted in Q1 by 1.6% and a model the Atlanta Fed uses, to track all of the inputs used by the BEA to calculate the official GDP number, has been projecting a negative number for Q2 since late June. That projection now stands at -1.6%, and we only have a few data points for the month of June yet to be incorporated. That data will come this week.

With that, by Thursday this week, we will get the first look at Q2 GDP. It will very likely be negative. Two consecutive quarters of negative GDP is by definition, a recession.

This is a technical recession, driven by high inflation (which is driven by both policy and pandemic driven supply deficits). But what does this technical recession really say about the health of demand?

If we look at the nominal rate of economic growth it's running hot - better than seven percent annualised based on the Atlanta Fed model.

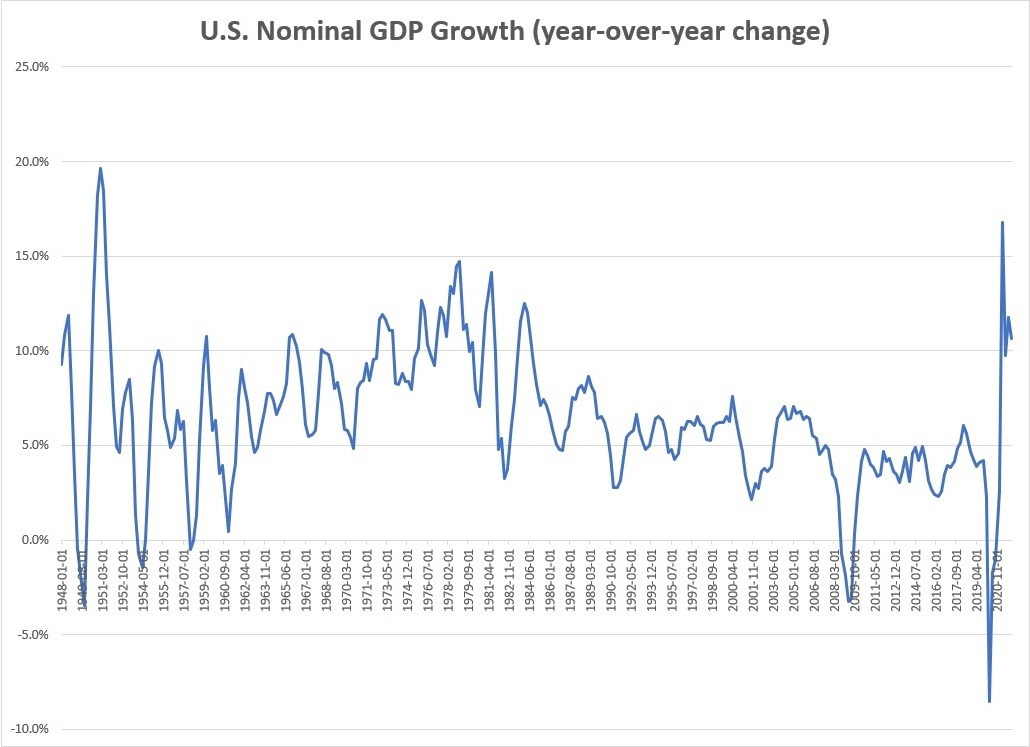

For perspective, take a look at the past seventy years of nominal GDP growth. This nominal growth rate is "rare air" for the U.S. economy, only seen in times of high inflation (which we are experiencing).

Of course, when we subtract a 9.1% year-over-year inflation rate, we get negative "real" GDP (i.e. after the effects of inflation). But that's all in the rear-view mirror, and aligns with a stock market that quickly discounted such a first half.

More importantly, what's in store for the second half of the year?

Heading into the first half of the year, the Fed was clearly going to embark on a new tightening cycle. A rising rates environment is a recipe for lower P/Es (lower valuation on stocks) - the P/E on the broad market has indeed fallen, from well north of 30 (ttm) to around 20.

Heading into the second half, there is a fair case to be made that this tightening cycle is near the end - perhaps as early as this week (with one more hike).

Add to this, the job market remains strong, with consumers and business balance sheets also remaining strong (as just confirmed in bank earnings reports).

This sets up for a good second half.

PS: If you know someone that might like to receive my daily notes, they can sign up by clicking below ...