A Global Summary

Macro Perspectives: Mon 15 Mar 2021

With not much happening in the markets on Friday and the weekend, I will use today's note to put down my thoughts from a global perspective.

Brazil’s Problem: alongside the U.S. fiscal stimulus, the second wave of COVID-19 in Brazil is likely to contribute strongly to upward pressure in the price of commodities (Iron ore, Soybeans, Sugar, Copper, etc). It seems that the world's biggest party - Carnival - a few weeks ago has made the situation worse and the death number has been increasing significantly since. Brasilia, the capital, went into lockdown at the start of the month to try to curb the pandemic enhanced by variants of SARS-Cov-2. As a result, the top commodity producer in the world has experienced harvest delays nationwide and shipping delays in its harbors.

Fixed Income: inflation has become the hot topic across MSM and it will be influencing institutions’ quarterly end rebalancing. Bond markets have been pricing in an acceleration of inflation (shown through Volatility in the chart below), due to vaccine rollout, easing health restrictions, high commodity prices and $1.9 trillion in stimulus aid. A significant reason for global central banks to control yield (by buying more bonds) is that federal, state, local, corporate and individuals all have too much debt to serve if interest rates increase.

Of note is the Reserve Bank of Australia doubling its bond purchases, trying to hammer down bets on reflation.

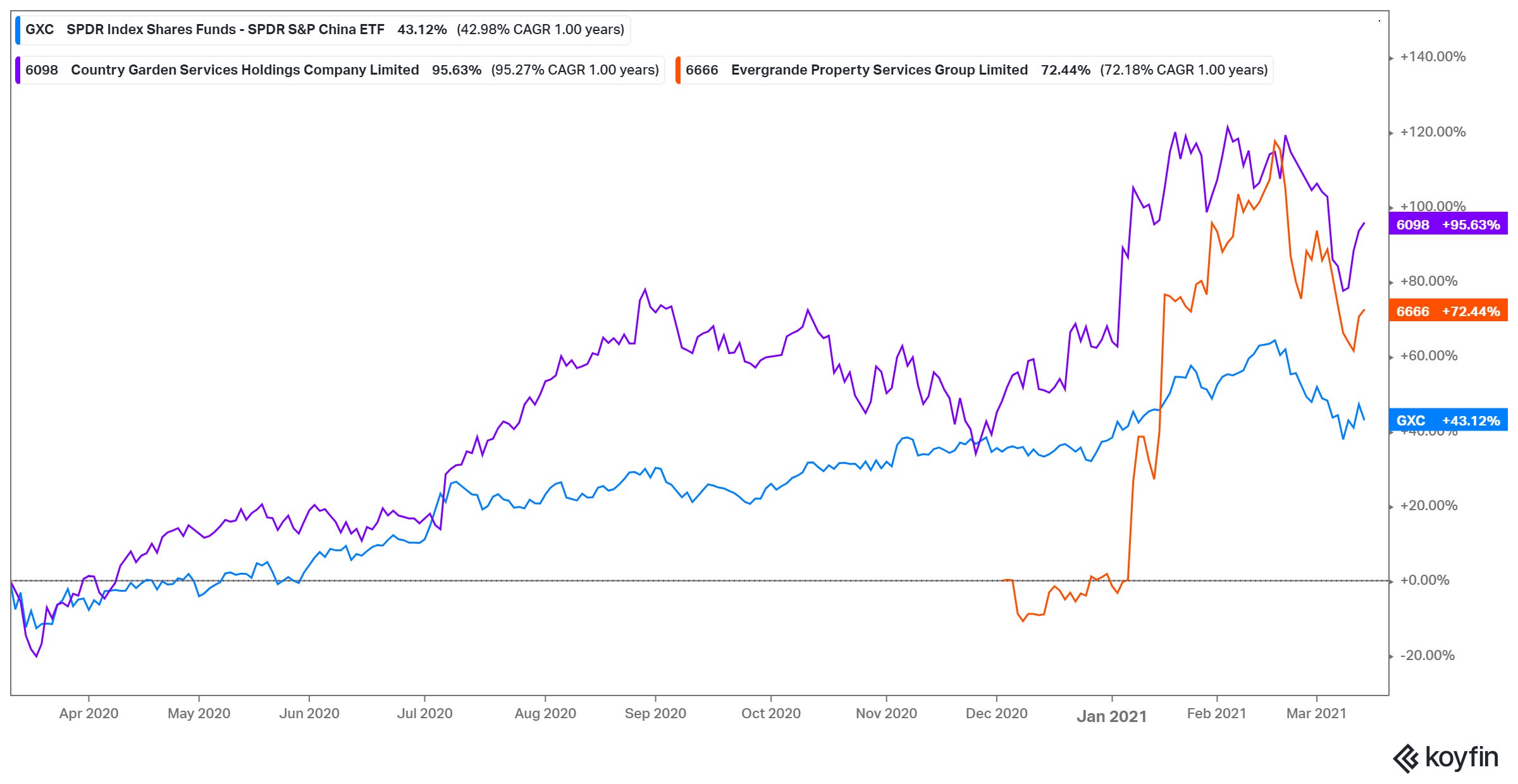

China: the U.S-Sino relationship has evolved into a more hostile atmosphere, despite Biden taking office. Recently, at the annual gathering of the Chinese People’s Political Consultative Conference (CPPCC), President Xi released a 5 year economic blueprint - The Dual-Circulation Strategy - whereby the government will scale back infrastructure spending (to temper financial risks and the property market bubble) as well as reduce China’s reliance on foreign goods and services. The odds for a continuing bull market seem increasingly slim.