3 Uncle Points followed by a Commodities Cycle?

Macro Perspectives

We've talked about the stress that rising global interest rates are putting on the global financial system, all being pulled along by U.S. monetary policy (and U.S. market interest rates).

The global financial system continues to show intolerance to higher interest rates, after a fourteen-year period of quantitative easing and zero interest rate policy.

Uncle Point 1: First, it was Europe's sovereign debt market that was breaking, as U.S. 10-year yields were hitting about 3.30%. The ECB had to intervene to avert a sovereign debt crisis.

Uncle Point 2: Then it was the UK bond market that broke. The Bank of England intervened to avert a financial system meltdown. The U.S. yields traded up to 4% when the UK bond market crisis was revealed (yet it was blamed on the new UK tax cut plan).

Uncle Point 3: Friday it was the Bank of Japan's turn. They intervened in the currency markets, defending the rapidly declining value of the yen.

This came after a 31% decline in the yen (on the year), relative to the dollar. It came as U.S. yields surpassed 4%, and climbed over the past three days, unabated, to 4.34%.

Of course, the weak yen is driven by divergent monetary policies of Japan and the U.S.. Money moves out of Japan (zero interest rates), and into the U.S. for a favorable yield, which also encourages a yen carry trade - borrowing yen (virtually free), selling it and buying dollars and earning about a 4% interest rate spread.

What does it mean for markets?

The BOJ intervention on Friday morning (EST) turned the tide of markets on the day: stocks higher, yields lower, commodities higher and the dollar broadly lower.

This also came with some Fed speak/news on the day, somewhat less hawkish than the drumbeat we've heard since the September meeting.

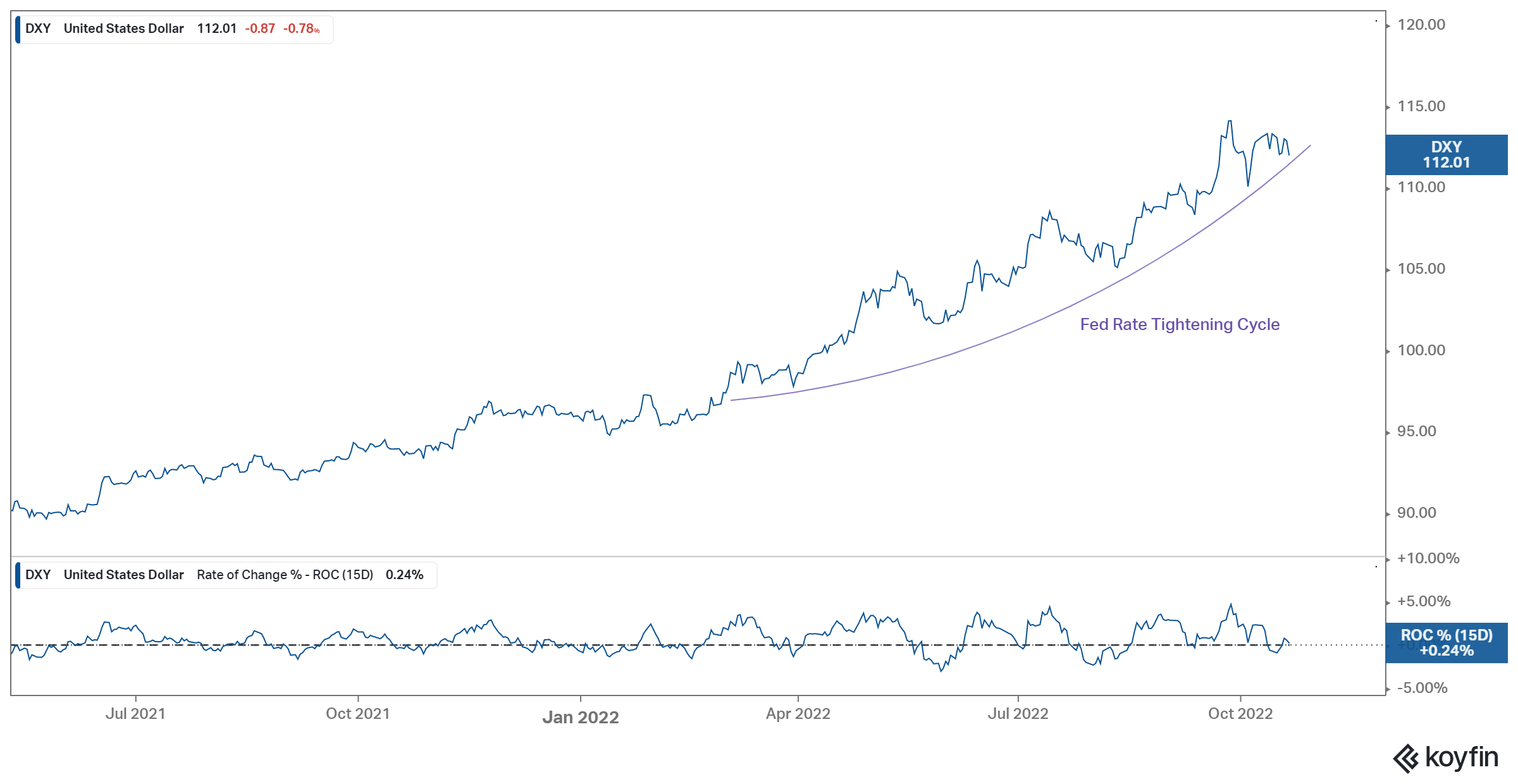

Nonetheless, this dollar chart, as we closed the week, becomes very important.

If the dollar trend is over, it will breathe new life into commodities prices.

A Message from the Sponsor.