16 Months to August

Stocks in the US finished near the flatline on Tuesday, as the S&P 500 added 0.1% to mark a 4-day winning streak, the Dow added 31 points, rising for the fifth straight day to post its longest win streak since December, while the Nasdaq edged lower by 0.1%.

Investor sentiment was cautious as they assessed whether the recent market rally could be sustained in light of the latest economic data.

Disney shares fell 9.5% after the company reported revenue that slightly missed forecasts and lower-than-expected overall Disney+ subscriber numbers.

Palantir Technologies saw its stock price drop 15.1%, its worst performance since May 2022, after issuing a weaker-than-expected outlook.

Peloton's stock surged 15.5% on news that private equity firms are considering a buyout of the fitness company.

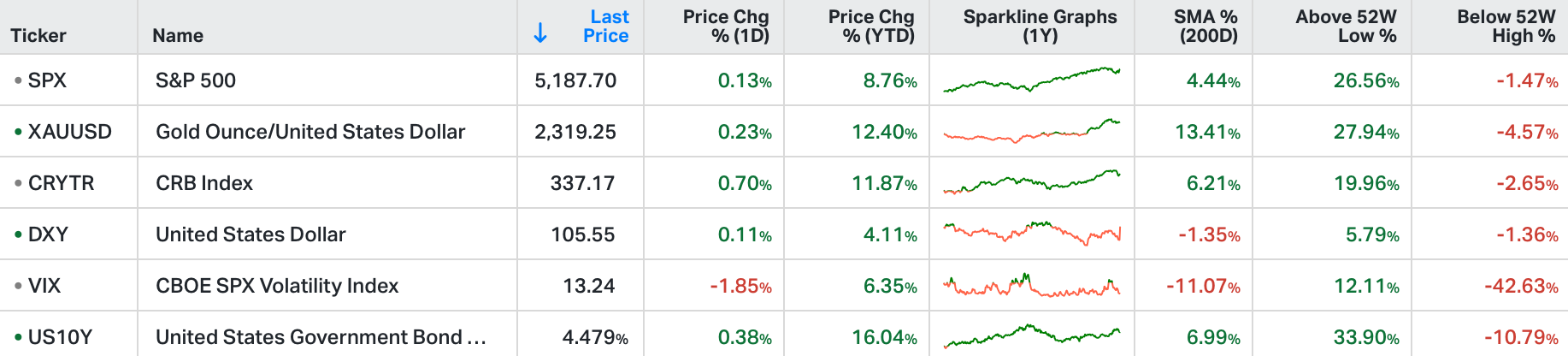

We talked yesterday about the bounce back in stocks, from what looks like a relatively shallow technical correction (7% in the S&P 500 index).

Shallow corrections are a sign of strength in a bull market - driven by durable tailwinds of a new industrial revolution AND the deployment of trillions of dollars in deficit spending.

We've also talked a lot about the outlook for an easing cycle for interest rates, which is another tailwind. The posturing on "when" it will commence, continues this week with a lineup of Fed members making the media rounds. But as we discussed in late March, if there were doubt on whether or not this easing cycle would materialize, the Swiss National Bank removed that doubt with its surprise rate cut in March.

As we discussed in that March note, the major central banks of the world have coordinated closely throughout the crises of the past 15 years. They all went to ultra-easy emergency level policies in response to the pandemic, and now all (except Japan) have interest rates set ABOVE the rate of inflation (restrictive territory). And we should expect them to all be cutting rates, in coordination, mostly to ensure that global liquidity doesn't become too tight, and (related) that their respective government bond yields (borrowing rates) don't run away (higher).

With that, the Bank of England meets tomorrow. Both the Bank of England and the European Central Bank are telegraphing the beginning of rate cuts in June. That's driving UK stocks back to new record highs whilst German stocks are less than one percent away from new record highs.

And we should expect the U.S. central bank and U.S. stocks to follow. But what about "sticky" inflation in the U.S.?

We had a growth shock in money supply (the green line), from the 2020-2021 policy response to the pandemic. That was the inflation catalyst. And you can see the lagging effect on inflation (red and blue lines), as it peaked 16 months after the peak of money supply growth.

We've since had the disinflationary effect (falling inflation) from the decline in money supply growth. Not only has money supply growth declined, it has contracted for sixteen consecutive months. Contracting money supply is historically deflationary.

If we apply the sixteen month lag of inflation to the trough in money supply growth, it would project much lower inflation data (maybe deflation) by August. If that's the case, the Fed will be cutting aggressively.

Keep in mind however, that, mirroring the Department of Justice’s “sixty-day rule” to not take prosecutorial steps that could influence an upcoming election, I suspect the FED will be loath to make any policy adjustments at their July and September meetings.